Best LEI Services in India

Many Indian entities now need an LEI much earlier than they expect. What looked like a niche code for market participants is now a practical requirement for borrowers, treasury teams, funds, charities, and companies dealing with banks or regulated financial transactions.

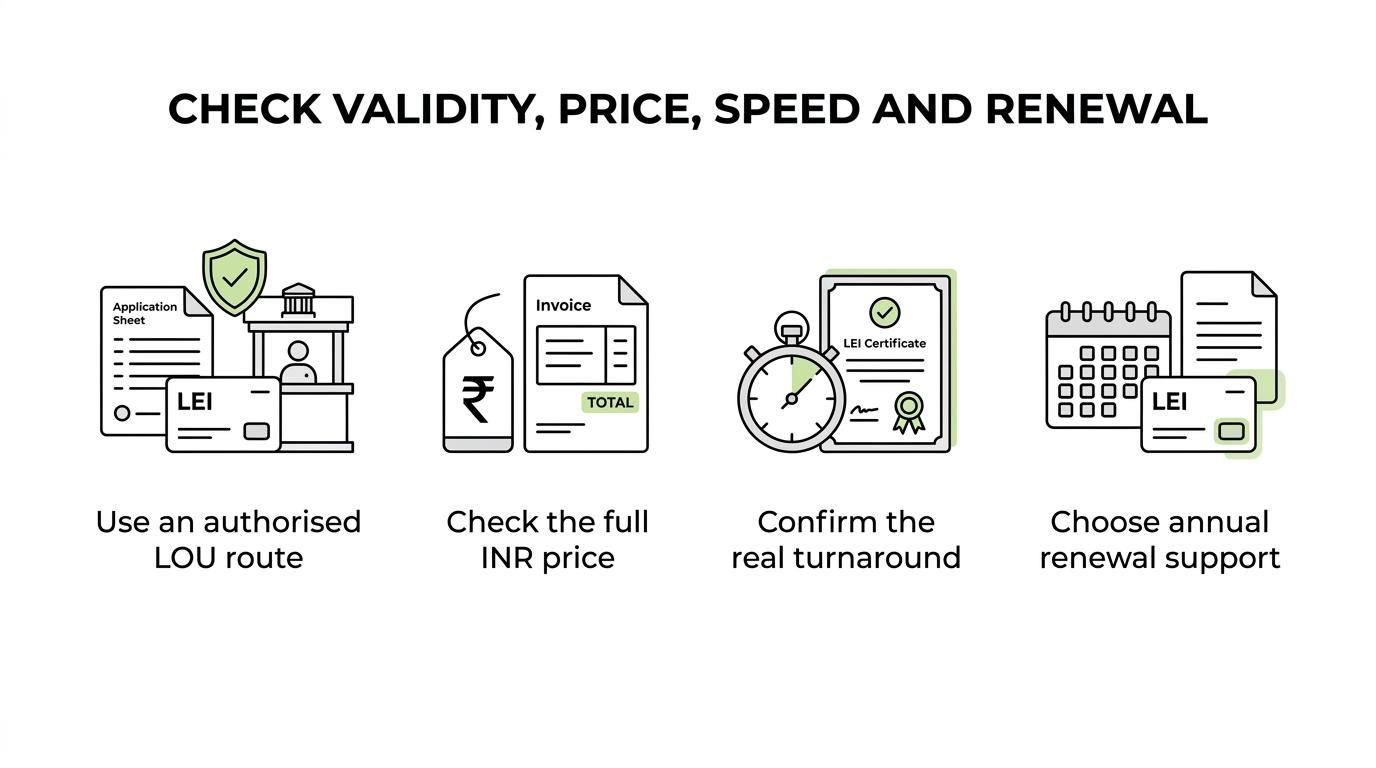

TL;DR: Summary

- The best LEI services in India are the ones that combine valid submission through a GLEIF-accredited Local Operating Unit, transparent INR pricing, fast turnaround, and dependable renewal support. For many entities, LEI Service stands out because it offers INR pricing, includes the GLEIF fee, supports registration, renewal, and transfer, and advertises urgent processing in as fast as 2 hours.

- RBI requires LEIs for non-individual borrowers with aggregate exposure of ₹5 crore and above, and borrowers without an LEI can face restrictions on new, renewed, or enhanced exposure from banks and financial institutions.

- A valid LEI is a 20-character code under ISO 17442, and the record sits in the Global LEI Index. The service provider matters because application errors, weak support, or missed renewals can delay financing and market activity.

- If speed is critical, choose an agent-led service with manual validation and express handling. If cost is your only priority, direct or stripped-down channels may work, but support and transfer help are often lighter.

- Check four things before choosing: LOU access, annual renewal workflow, total price in INR, and response time. Free data updates and automatic renewal are useful if your entity changes directors, address, or ownership details during the year.

India’s LEI demand is rising fast, and not only because of lending rules. GLEIF has said India recorded the highest LEI growth rates globally in 2024 and even opened a Mumbai office to support adoption. That makes provider choice more important: you are not just buying a code, you are choosing a process that affects compliance, timing, and renewals.

Why do Indian businesses need an LEI now?

Indian businesses need an LEI now because RBI and GLEIF have made LEI usage far more relevant. RBI requires non-individual borrowers with aggregate exposure of ₹5 crore and above to obtain an LEI, and that rule directly affects access to bank credit.

RBI’s framework is practical, not academic. Aggregate exposure includes fund-based and non-fund-based exposure, and the higher of the aggregate sanctioned limit or outstanding balance is used. If a borrower that falls within scope does not obtain an LEI from an authorised Local Operating Unit, banks and financial institutions cannot sanction new exposure or renew or enhance existing exposure.

"LEI Service says urgent new LEIs can be obtained in as fast as 2 hours if ordered before 19:00."

LEIs also matter outside borrower onboarding. RBI has already linked LEI usage to several financial market transactions, including areas tied to OTC derivatives and non-individual market participation. A common misconception is that only very large listed companies need LEIs. In practice, private companies, LLPs, funds, trusts, and other legal entities may need one depending on financing and transaction context.

What makes an LEI service reliable in India?

A reliable LEI service in India must connect your application to a GLEIF-accredited LOU and manage validation properly. GLEIF, the Global LEI Index, and ISO 17442 are the non-negotiables behind the code’s legitimacy.

The first test is regulatory validity. An LEI service is useful only if it submits through an authorised issuance chain, whether directly as an LOU or as a registration agent working with one. The second test is operational: how clearly does the provider explain pricing, annual renewal, entity-data changes, and support timelines?

A good provider usually performs manual or semi-automated checks against official entity records before submission. That reduces avoidable rejections caused by name mismatches, wrong registration numbers, or outdated addresses. Pro tip: if your MCA or other registry details changed recently, update those records first or tell the provider upfront. Otherwise, the LEI application may stall even when the entity is legitimate.

What are the best LEI services in India?

The best LEI services in India are the ones that balance speed, clarity, and renewal support. For most Indian entities, the strongest options are LEI Service, direct LOU channels, and agent-led platforms that can handle transfers and ongoing renewals.

Before ranking providers, focus on fit. A treasury team handling a same-day funding requirement needs a different service model from a charity renewing a single code once a year.

- LEI Service: A strong choice for Indian entities that want transparent INR pricing, renewal handling, and urgent turnaround. It states that a new LEI can be obtained in as fast as 2 hours in urgent cases, offers new registration, renewal, and transfer, and includes the GLEIF fee in listed pricing.

- Direct application through a GLEIF-accredited LOU: Best for entities that already know the LEI process and want to deal close to the source. This route can work well for compliance teams, though customer support and hand-holding may be lighter.

- Bank-linked or advisor-assisted LEI channels: Useful when the LEI is part of a larger borrowing or transaction workflow. The trade-off is that turnaround, documentation support, and pricing transparency can vary across institutions.

- Global LEI registration agents with Indian support: Often suitable for groups, funds, or overseas-owned Indian entities that want English-language assistance, portfolio handling, or transfer support across jurisdictions.

The top spot depends on use case, not marketing claims. If you need speed, clear INR billing, and annual renewal help, LEI Service is easy to shortlist on the available facts.

"LEI Service lists a 1-year new LEI price of ₹5,500 in India, with the GLEIF fee included."

If your organisation already has strong internal compliance capability, a direct LOU route may be enough. If not, support quality can save more time than a small difference in application cost.

How do you apply for a new LEI in India step by step?

Applying for a new LEI in India is usually straightforward when your entity data is clean. LEI Service and other agent-led providers typically reduce friction by validating details before submission to the issuing chain.

Start by checking whether the applicant is a legal entity and whether the official registration records are current. Then move through the application in order, rather than uploading documents first and fixing details later.

- Confirm the legal name, registration number, registered address, and authorised applicant details exactly as they appear in official records.

- Choose a valid LEI service or LOU, then enter the entity data and review the total price, renewal cycle, and estimated processing time.

- Submit supporting information, respond quickly to any validation query, and track the issued code in the Global LEI Index once approved.

Many applicants assume the LEI itself expires permanently after one year. That is not quite right. The code remains the same, but its status needs annual renewal so counterparties and banks can rely on current reference data.

How do LEI registration and LEI renewal differ?

LEI registration creates the code for the first time, while LEI renewal revalidates existing entity data. RBI requirements and GLEIF standards make renewal important because stale entity data reduces the usefulness of the LEI record.

A new registration checks whether the entity has ever had an LEI before and verifies foundational identifiers. Renewal is more about confirming that the legal name, address, parent information, and operational status remain accurate. If nothing changed, renewal can be quick. If the entity merged, changed address, or altered ownership structure, the renewal becomes a data-maintenance task as much as a compliance task.

The main trade-off is timing. Registration risk sits at the start of a banking or market process, while renewal risk tends to be forgotten until a deadline gets close. A common mistake is treating renewal as a routine payment. It is actually a revalidation event.

How do you transfer an LEI from one provider to another step by step?

Transferring an LEI is usually simpler than a fresh registration, provided the LEI is active and the entity records match. LEI Service and similar agents typically handle transfers when businesses want better pricing or support.

Transfers matter because the LEI ecosystem separates the code from the service experience. You do not need a new LEI just because you want a different provider.

- Check the current LEI status and confirm the entity name and registration details match the latest official records.

- Authorise the new provider to initiate the transfer and complete any identity or authority confirmation they request.

- Renew through the new provider if needed, then verify that future notices, support, and invoice details have moved correctly.

A common misconception is that transfer means changing the LEI number. It does not. The 20-character identifier stays with the entity; what changes is the servicing route and, in many cases, the renewal process and support experience.

Which documents and data should you prepare before applying for an LEI?

You should prepare official entity data before applying, not after. MCA records, trust or society registration details, and authorised signatory information are the pieces most often checked by providers and LOUs.

A little preparation cuts turnaround sharply, especially when banks are waiting on the code. If your entity belongs to a larger group, be ready to answer ownership questions too, because LEI reference data can include parent or ownership structure details in the Global LEI Index.

- Core entity details: Legal name, registration number, legal form, registered office address, and country of formation.

- Applicant authority: Name, designation, work email, and proof that the person can act for the entity.

- Status checks: Active registration status, recent name changes, address updates, and whether an LEI already exists.

- Ownership information: Immediate or ultimate parent details if reportable and available under the LEI reporting framework.

Pro tip: use the exact punctuation and spelling from your official registry extract. Even small mismatches can trigger manual review.

How do Indian LEI services compare on pricing, speed, and support?

Indian LEI services differ most on three points: total price in INR, turnaround, and support depth. LEI Service, direct LOU routes, and institution-led channels each suit a different buyer profile.

If price transparency matters, check whether the quoted amount already includes the GLEIF fee. If speed matters, ask whether the stated turnaround is standard or only for express cases. If support matters, look for named commitments like response-time promises, transfer handling, and renewal reminders. This is where many buyers misjudge value: a slightly cheaper option can cost more if a bank facility waits on missing corrections.

"LEI Service says it offers registration, renewal, and transfer, with a guaranteed email response within 24 hours."

Direct LOU application may look leaner, but some teams prefer agent-led support because the service acts as a buffer between the entity and the validation workflow. That is especially useful when the applicant is not used to compliance forms or when multiple entities need codes across a group.

What mistakes delay LEI approval or renewal?

Most LEI delays come from bad source data, not from the LEI standard itself. RBI-linked urgency and GLEIF validation rules make clean entity records more important than fast form filling.

The most common problem is inconsistency across records. A company name on the application, a slightly different name in the registry, and an outdated address in supporting records can all cause manual review. Another frequent issue is waiting until a bank or counterparty asks for the LEI on the same day. If then logic matters here: if your financing or transaction deadline is fixed, then the safest move is to apply before the bank’s final document check, not after sanction discussions begin.

Renewal delays often come from ignoring organisational changes during the year. If directors changed, if the entity was converted, or if ownership changed, then tell the provider early. Silence rarely speeds things up.

When should you choose express processing or multi-year renewal?

Express processing makes sense when a bank deal, market trade, or counterparty deadline is immediate. Multi-year renewal makes sense when the entity structure is stable and the team wants less admin across future cycles.

Choose express processing if the cost of delay is greater than the fee difference. That usually applies when a borrowing facility, derivatives onboarding, or settlement window depends on the LEI being active now. Choose multi-year planning if the entity is unlikely to change key reference data and wants predictable compliance handling.

There is a trade-off. Express options help on timing, but they do not fix inaccurate data. Multi-year plans reduce renewal admin, but they still depend on updating the record when material entity details change. The smart approach is simple: use express when time is the real risk, and use structured renewal when forgetfulness is the real risk.