LEI for OTC Derivatives in India

For Indian entities active in over-the-counter derivatives, the Legal Entity Identifier is not a back-office extra. It is tied to market access, trade reporting, and the basic ability to participate in certain regulated OTC derivative segments.

That point matters for a wide set of participants. A large treasury desk using foreign currency forwards, a company hedging interest rate exposure, a fund entering into derivative contracts, or a financial institution reporting transactions all need to treat the LEI as part of their operating readiness.

The Indian framework is also connected to a global identification system. The code itself follows an international standard, while local market infrastructure and regulatory rules determine when it must be in place and kept active. For OTC derivatives in India, those pieces come together very clearly.

Why LEI is a regulatory requirement for OTC derivatives in India

The Reserve Bank of India set out the LEI requirement for participants in specified OTC derivative markets through its notification dated 1 June 2017. The requirement was introduced in a phased manner for all participants in the OTC markets for rupee interest rate derivatives, foreign currency derivatives, and credit derivatives in India.

The practical message is direct. An entity without an LEI is not eligible to participate in the relevant OTC derivative markets after the date applicable to it under the RBI schedule. That makes the LEI more than a reference number used for record-keeping. It becomes part of the eligibility framework for trading.

For market participants, this changes how compliance should be viewed. LEI readiness needs to be checked before a hedging programme is launched, before onboarding with a dealer, and before reporting processes are tested.

- Market access

- Counterparty identification

- Trade repository reporting

- Regulatory readiness

- Ongoing renewal control

A common mistake is to think the requirement affects only banks or very large corporates. In reality, the key question is whether the legal entity participates in the OTC derivative segments covered by the RBI framework.

What the LEI code means under the global LEI standard

The LEI is a 20-character alphanumeric code under ISO 17442, the global standard used for the Legal Entity Identifier system. It is designed to identify legally distinct entities that enter into financial transactions.

That standardisation matters because OTC derivatives often involve multiple systems, counterparties, repositories, and supervisors. A single globally recognised identifier reduces confusion caused by name variations, mergers, abbreviations, or cross-border registrations. When a legal entity is identified in a uniform way, data quality improves across the trade lifecycle.

The code is also linked to reference data about the entity. That can include the official legal name, registered address, country of formation, and other core data used to identify the entity accurately. Since this reference data can change, the LEI is not a one-time set-up that should then be forgotten.

- Format: 20-character alphanumeric code based on ISO 17442.

- Entity focus: Issued to legal entities rather than natural persons.

- Data link: Connected to verified reference data about the entity.

- Renewal cycle: Re-validation is required at least once each year.

- Status value: An active LEI is far more useful operationally than a lapsed one.

Annual renewal is often underestimated. GLEIF states that legal entities and LEI issuers must re-validate legal entity reference data at least once per year. In market terms, that means a code may continue to exist, but if it is not renewed, its status can become a weak point in onboarding, reporting, or internal compliance reviews.

How CCIL trade repository reporting uses the LEI

In India’s OTC derivatives environment, the LEI is closely connected to reporting infrastructure. The Clearing Corporation of India Limited, or CCIL, acts as a designated trade repository authorised by RBI under the Payment and Settlement Systems Act, 2007 to collect, collate, store, maintain, process, and disseminate data related to specified OTC derivative transactions.

CCIL’s OTC derivatives trade repository rules define the LEI as a 20-character unique identity number assigned to entities that are parties to a financial transaction under the global LEI system. That definition is not incidental. It shows that the LEI is built into the identification logic of trade reporting.

When trades are reported to a repository, the parties to the transaction must be captured consistently. A common identifier allows the repository to match, process, and organise data more reliably. It also supports better supervision and market visibility.

That is why a missing or expired LEI can create friction even when the commercial terms of a trade are settled.

| OTC derivatives LEI checkpoint | What it means in practice | Why it matters |

|---|---|---|

| Before trade execution | Confirm the correct legal entity has its own LEI | Avoids last-minute trading blocks |

| Counterparty onboarding | Share an active LEI with the dealer or bank | Speeds up KYC and static data checks |

| Trade repository reporting | Use the LEI as the defined entity identifier | Supports accurate reporting to CCIL systems |

| Annual maintenance | Renew the LEI on time | Keeps reference data validated |

| Entity changes | Update legal name, address, or registration details | Prevents mismatches across systems |

For treasury and compliance teams, the operational lesson is simple. The LEI should sit inside the same control framework as authorisations, static data, and reporting templates.

Which Indian entities should arrange an LEI before OTC derivatives activity

Any legal entity planning to participate in covered OTC derivative markets should check its LEI status well before execution. That includes corporates hedging currency or interest rate exposure, financial institutions, funds, and other organised entities entering into regulated derivative transactions.

Each legal entity needs its own LEI.

This point matters in group structures. A parent company’s LEI does not substitute for a subsidiary’s LEI if the subsidiary is the actual contracting party. If a treasury centre, SPV, fund vehicle, or operating company enters into the derivative, that specific entity’s identifier must be correct and active.

A good internal review usually includes these checks:

- Confirm which exact legal entity signs the OTC derivative contract.

- Match the legal name and registration details to official records.

- Verify that the LEI is active and due for renewal only after the intended trading window.

- Check whether any recent corporate changes need to be updated in the LEI record.

This review is especially useful for entities that trade only occasionally. A business that enters derivatives once or twice a year can still be caught out by an expired code or by entity data that no longer matches current records.

How LEI registration and renewal usually work for Indian entities

RBI has stated that LEIs may be obtained from Local Operating Units accredited by GLEIF, and that in India they may be obtained from Legal Entity Identifier India Ltd. which RBI recognised as an LEI issuer. In practice, many entities also use registration agents that handle document checks, validation, and submission to a GLEIF-accredited issuer.

The application itself is usually straightforward when entity records are in order. The key work lies in validating the legal entity data accurately. Applicants are generally asked for details such as the official legal name, registered address, registration number, and supporting evidence that the requester is authorised to apply on behalf of the entity.

Entities should also remember that an LEI record needs maintenance after issuance. If the legal name changes, the registered office changes, or the entity is affected by a merger or restructuring, the data should be updated.

LEI renewal is as important as first-time issuance

A first registration solves only one part of the requirement. Since the LEI system depends on periodic re-validation, renewal needs to be treated as a scheduled compliance task.

That is where operational habits matter. Entities that depend on derivatives for hedging often prefer not to leave renewal to the last minute, especially when quarter-end activity, audit work, or refinancing events already place pressure on internal teams. An automatic renewal option can be helpful in that setting, provided someone remains responsible for reviewing entity data when changes occur.

LEI pricing and service options for Indian market participants

Published INR pricing from LEI Service for new LEI registration lists the following rates, with the GLEIF fee included:

| LEI registration term | Published price in INR | Notes |

|---|---|---|

| 1 year | ₹5,500 | GLEIF fee included |

| 3 years | ₹15,600 | GLEIF fee included |

| 5 years | ₹24,500 | GLEIF fee included |

For entities that prefer a simple process, service features can matter as much as price. LEI Service states that it offers a one-minute application, processing as fast as 2 hours, guaranteed email response within 24 hours, optional automatic renewal, English-speaking support, and free updates to entity data. It also states that it is an official LEI registration agent of Ubisecure RapidLEI.

That sort of service model may appeal to businesses that want a fast turnaround before a planned trade, a renewal cycle that does not depend on memory alone, or support in English without extra friction.

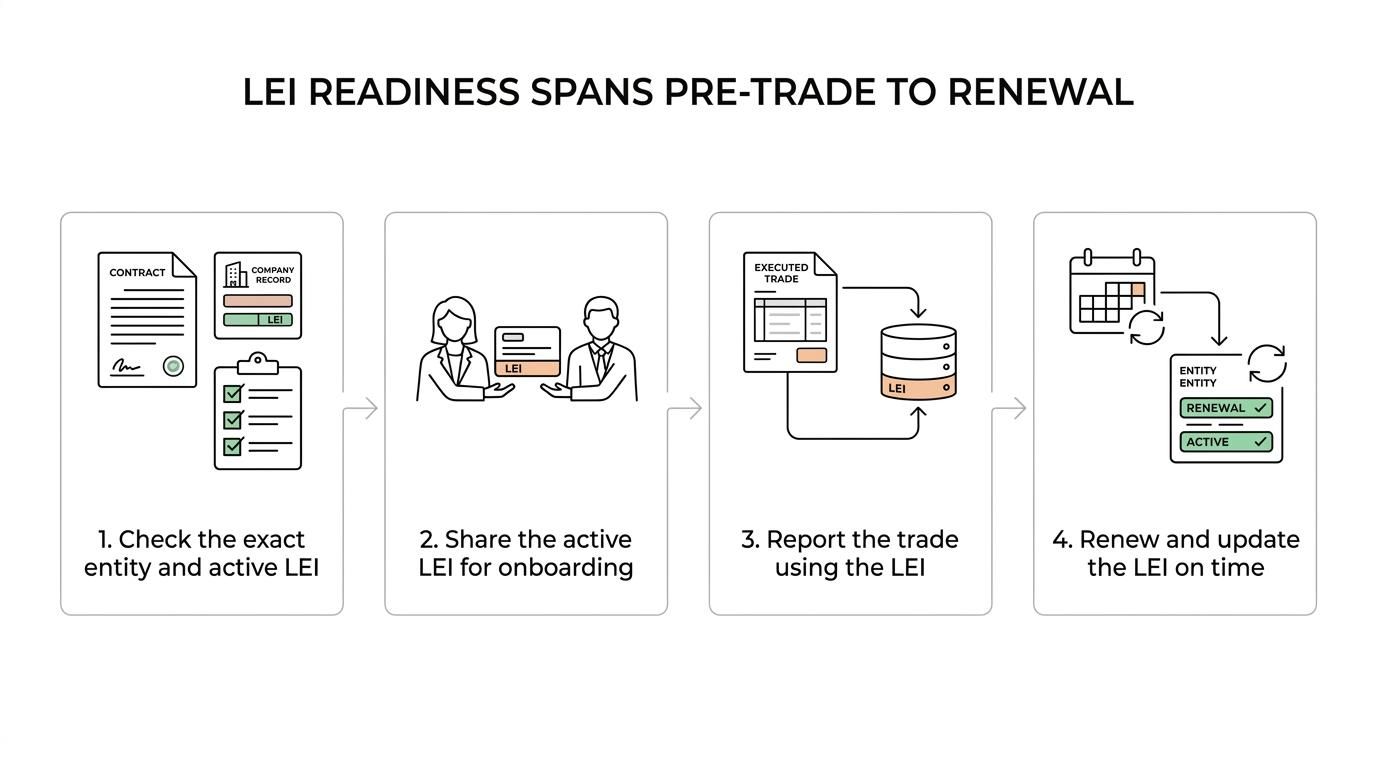

Practical LEI steps before your next OTC derivatives trade

A useful approach is to treat the LEI like any other pre-trade control item. If your entity is new to OTC derivatives, secure the code before documentation and onboarding reach the final stage. If your entity already has a code, check the renewal date before the next hedge, not after the term sheet is agreed.

It is also sensible to map LEI responsibility internally. Treasury may need it for execution, compliance may need it for policy checks, operations may need it for reporting, and finance may need visibility on renewal dates and invoices. When nobody owns the task, the risk rises quickly.

For entities trading in rupee interest rate derivatives, foreign currency derivatives, or credit derivatives in India, the LEI sits at the intersection of regulation, reporting, and practical market access. Keeping it active and accurate is one of the clearest ways to avoid preventable disruption.