LEI for RTGS Above Rs 50 Crore

When a non-individual entity in India plans a very large bank transfer, the LEI is not a nice-to-have detail. It is often the difference between a smooth payment and a transaction that stalls at the bank review stage.

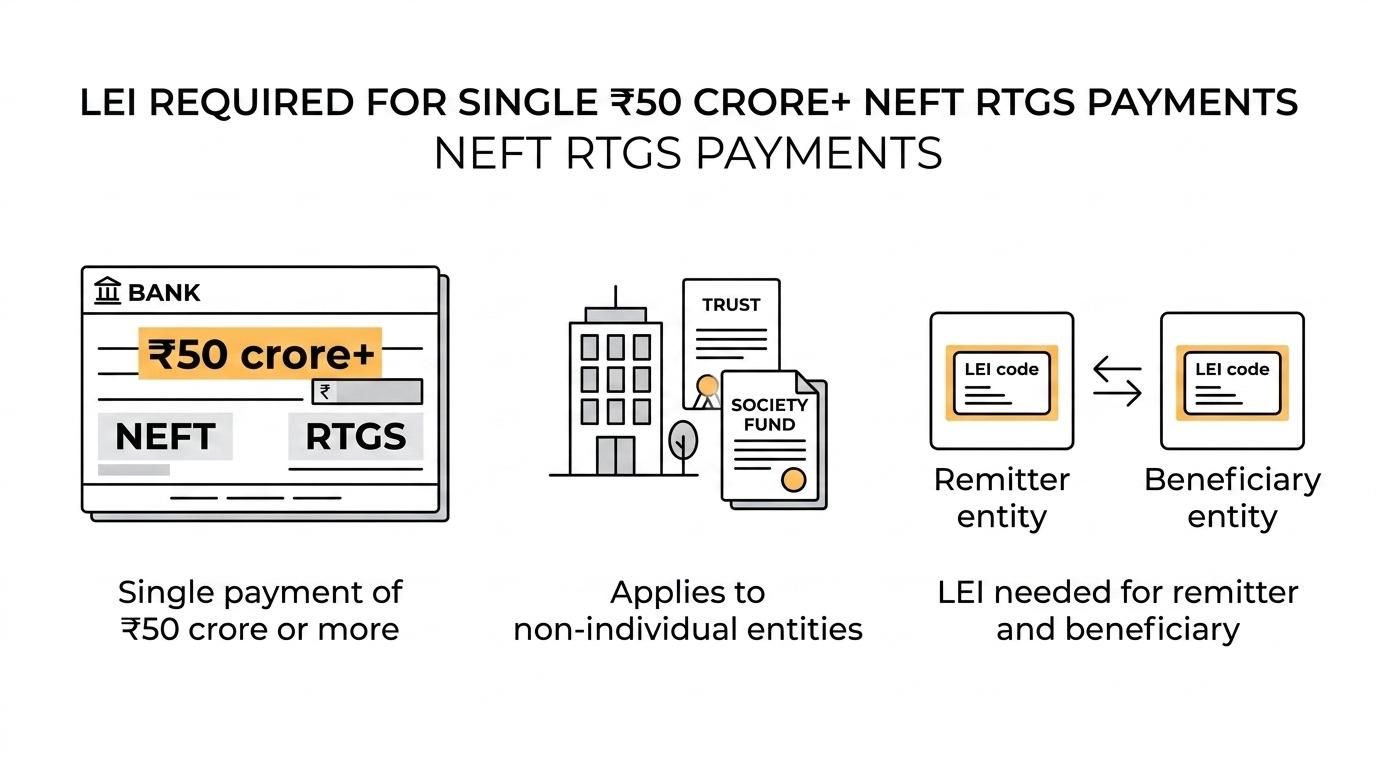

For single NEFT or RTGS payments of ₹50 crore and above, the Reserve Bank of India requires LEI information for both the remitter and the beneficiary where the parties are non-individual entities. That makes advance preparation essential for companies, LLPs, trusts, societies, funds, charities, government undertakings, and other legal entities that move large sums through the banking system.

RBI rule for LEI in RTGS and NEFT above ₹50 crore

The RBI requirement applies to all single payment transactions of ₹50 crore and above undertaken by non-individual entities through NEFT and RTGS. In plain terms, if a legal entity is sending or receiving one such payment, the LEI data has to be part of the transaction information.

This is not limited to one narrow type of RTGS use case. For RTGS, the rule covers both customer payments and inter-bank transactions that meet the threshold.

That scope matters because many finance teams still assume LEI is relevant only to capital markets, derivatives, or bank borrowing. In this case, it directly affects high-value payment operations. If the payment crosses the threshold, LEI becomes a compliance requirement.

A few points make the RBI position easier to apply in practice:

- Threshold test: single payment transaction of ₹50 crore or more

- Payment systems covered: NEFT and RTGS

- Parties covered: non-individual entities

- LEI data required: remitter and beneficiary LEI information

- RTGS coverage: customer payments and inter-bank transactions

The exemption side is just as important. Government Departments and Ministries do not need an LEI for these NEFT and RTGS payment transactions. Government Undertakings and Corporations, including fully owned ones, do need an LEI if they are making or receiving single payment transactions at or above the threshold.

Which entities need LEI for large-value RTGS payments

Many organisations ask the same practical question: “Does this apply to us?” The answer depends less on industry labels and more on legal status and transaction type.

If the entity is a non-individual legal person and it is involved in a single RTGS or NEFT payment of ₹50 crore or more, the requirement is likely relevant. That is why the rule reaches far beyond listed companies and large banks.

The entities commonly affected include the following:

- Private and public companies

- LLPs and partnerships where applicable as legal entities

- Trusts

- Societies

- Charities

- Funds

- NBFCs

- Government undertakings and corporations

A quick reference table can help finance, treasury, and compliance teams decide faster.

| Entity type | LEI needed for single RTGS/NEFT of ₹50 crore and above? | Notes |

|---|---|---|

| Private limited company | Yes | Non-individual entity |

| Public company | Yes | Non-individual entity |

| LLP | Yes, where treated as a legal entity for the transaction | Bank validation may check entity records |

| Trust | Yes | Common trigger for donor, corpus, or asset transfers |

| Society | Yes | Applies if making or receiving qualifying payments |

| Charity / non-profit entity | Yes | Rule follows the transaction and entity status |

| Government Department / Ministry | No | RBI FAQ provides exemption |

| Government undertaking / corporation | Yes | Includes fully owned undertakings |

| Bank in inter-bank RTGS | Yes | Applies where threshold conditions are met |

This is why internal assumptions can be risky. A trust making a one-time property settlement, a society receiving a major grant, or a corporate treasury moving funds within a business structure may all meet the same payment threshold and face the same LEI requirement.

What an LEI code contains and why banks verify it

An LEI is a 20-character alphanumeric code that identifies a legal entity in a standard global format. It links to verified reference data drawn from authoritative sources, and that can include information about ownership structure.

That may sound technical, but the business value is straightforward. The code helps banks identify exactly who is sending and receiving large-value funds. It reduces ambiguity, supports screening, and improves record quality across institutions.

Banks are also expected to maintain valid and verified LEI information for payment transactions above the threshold after credit. That means the LEI should not only exist, it should also be current.

A valid LEI usually helps with three things at once:

- Payment processing: banks can capture remitter and beneficiary details in the required format

- Compliance checks: entity identity is easier to confirm against verified records

- Future transactions: once the LEI is active and renewed on time, repeated large-value payments become easier to manage

This is one reason many entities now treat LEI as part of treasury readiness rather than a one-off administrative task.

How to get an LEI before an RTGS transaction

Waiting until the payment date can create pressure that nobody wants. A large RTGS transfer often involves internal approvals, beneficiary confirmation, bank coordination, and cut-off times. Adding urgent LEI registration at the last minute is avoidable.

The cleaner approach is to arrange the LEI as soon as a high-value payment becomes likely.

In most cases, the application process is built around basic legal entity data and supporting evidence. A registration agent submits the application to a GLEIF-accredited Local Operating Unit, often called an authorised LOU, after validation.

Typical application inputs may include the following:

- Registered legal name: exactly as shown in official records

- Entity registration details: incorporation or registration number, where applicable

- Registered address: matched with source documents

- Authorised contact details: email and phone for validation queries

- Supporting documents: paperwork that confirms the entity’s legal existence and current data

Accuracy matters here. Even small mismatches between the application and official records can slow validation. Entity name variations, old addresses, or outdated registration details are common reasons for back-and-forth checks.

Some providers focus on keeping this simple. LEI Service, for example, offers a one-minute application flow, English-speaking support, and validation handling for new registrations, renewals, and transfers. For urgent cases, express processing may be available as fast as 2 hours, which can be useful when a payment deadline is close.

LEI registration and RTGS payment readiness should be planned together

An LEI on its own does not complete the payment instruction. The bank still needs the right transaction data, and the remitter and beneficiary details need to be consistent with the payment records.

That is why treasury teams often coordinate three moving parts together: the entity’s valid LEI, the beneficiary’s LEI, and the payment instruction fields used by the bank.

A practical internal checklist often includes:

- Confirm the payment is a single transaction of ₹50 crore or more

- Confirm both parties are non-individual entities

- Check whether both LEIs are active and current

- Verify names and records match bank-held details

- Share LEI information with the bank before payment initiation if needed

For recurring corporate payments, this preparation can save real time. It also reduces the chance of same-day escalation between treasury, operations, relationship managers, and compliance teams.

LEI pricing, timelines, and renewal options in India

Cost is usually modest compared with the size of the transaction it supports. For most entities, the more relevant question is not whether to get an LEI, but how quickly and how neatly the process can be completed.

On India-facing pricing pages, LEI Service lists these INR rates for registration and renewal, with the GLEIF fee included:

| Term | Price |

|---|---|

| 1 year | ₹5,500 |

| 3 years | ₹15,600 |

| 5 years | ₹24,500 |

Multi-year options can make planning easier for entities that expect regular high-value payments or ongoing regulatory use of the LEI. They also reduce the risk of forgetting annual renewal.

Renewal deserves attention because an expired LEI can create the same operational problem as having no LEI at all for a payment that requires valid and verified LEI information. Automatic renewal options are useful for entities with lean finance teams or several compliance deadlines across the year.

The service model can matter just as much as the sticker price. Fast turnaround, transparent INR pricing, included GLEIF fees, free updates to entity data, and a guaranteed email response within 24 hours can make the process easier for Indian entities that want a predictable route from application to active code.

Common mistakes with LEI for RTGS above ₹50 crore

Most problems are preventable. They usually come from assumptions made too late in the payment cycle.

A frequent mistake is assuming only the sender needs an LEI. The RBI rule requires remitter and beneficiary LEI information for covered transactions, so both sides should be checked early.

Another issue is confusing a large total relationship value with the actual payment threshold. The rule discussed here is tied to a single payment transaction of ₹50 crore or more through NEFT or RTGS.

Teams also run into trouble when the LEI exists but is not current. Banks look for valid and verified information, not only a historical code on file.

The patterns are familiar:

- Late application: LEI requested only after the payment is queued

- Data mismatch: entity name or address does not match official records

- Renewal gap: code exists but has lapsed

- Wrong scope assumption: belief that trusts, societies, or charities are outside the rule

- One-sided preparation: remitter ready, beneficiary LEI missing

For entities that may need to move large funds at short notice, early registration is usually the best operational decision. It keeps the focus where it belongs: on executing the payment, not scrambling for identity documentation at the last minute.

A valid LEI is a small code with a very large practical effect when ₹50 crore or more is moving through RTGS or NEFT.