Parent-Subsidiary Relationships in LEI Records: Direct vs Ultimate Parent Explained

When an Indian entity applies for an LEI, one part of the form often creates more confusion than expected: parent information.

Many people assume this is a simple ownership question. Who owns the shares? Who controls the board? Who is the promoter? In LEI records, the answer is narrower and more technical. The LEI system uses an accounting consolidation lens for parent reporting, not every possible form of legal or economic control.

That distinction matters. If a company reports the wrong parent, its LEI application or renewal may need extra validation, and the resulting record may not reflect the group structure in the way regulators and market participants expect.

Direct parent vs ultimate parent in LEI records

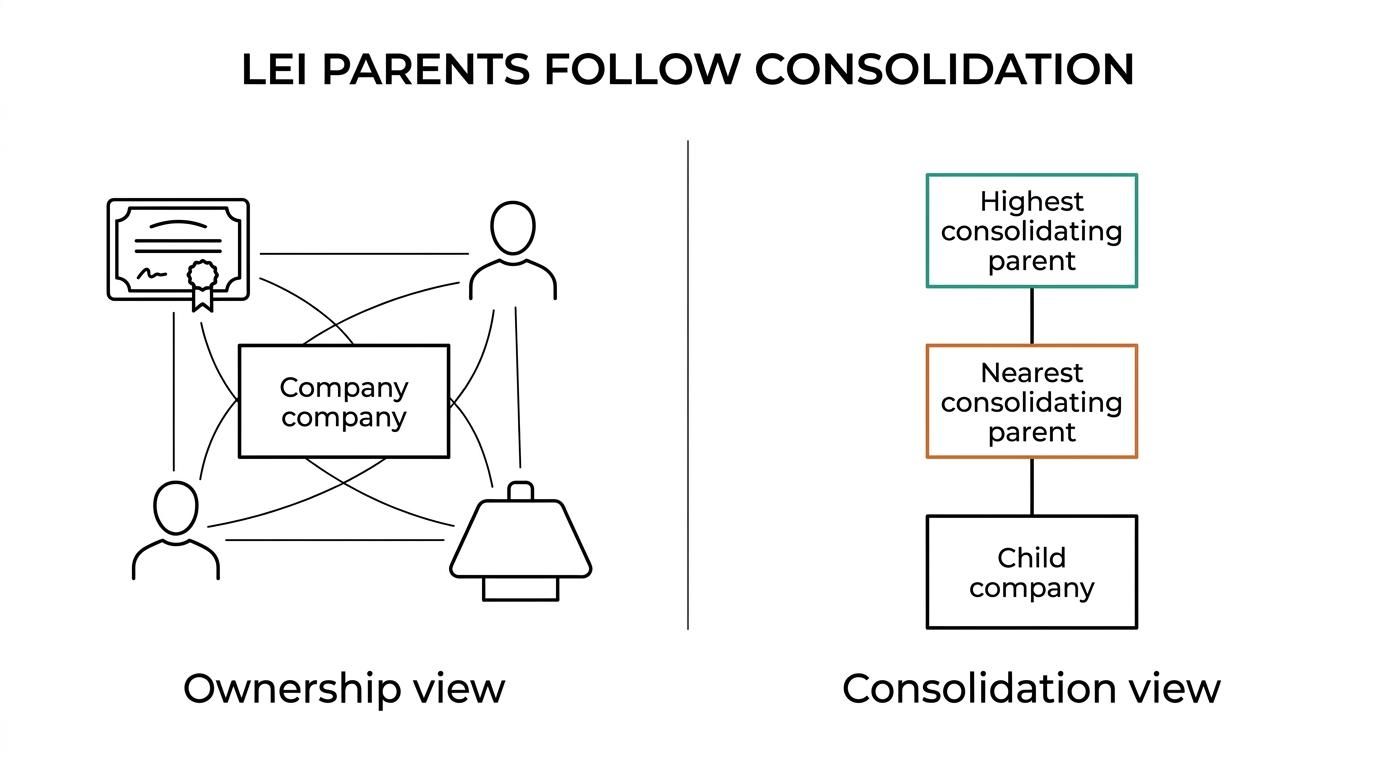

In LEI data, a direct parent is the closest legal entity that consolidates the child into its financial statements. An ultimate parent is the highest legal entity in the chain that prepares consolidated financial statements including that child.

So the key test is not simply shareholding. The key test is whether the entity sits inside consolidated accounts, and where it sits in that reporting chain.

A quick example makes this easier. Imagine Company A in India is fully consolidated by Company B, and Company B is in turn fully consolidated by Company C at the top of the group. In that structure, Company B is the direct parent, while Company C is the ultimate parent.

| Aspect | Direct Parent | Ultimate Parent |

|---|---|---|

| Position in the group | Closest consolidating parent | Highest consolidating parent |

| LEI meaning | Immediate accounting consolidation link | Top accounting consolidation link |

| Can both exist at once? | Yes | Yes |

| Can they be the same entity? | Yes, if the nearest parent is also the top parent | Yes |

| Is it based on any ownership link? | No, it is based on consolidation | No, it is based on consolidation |

This is why LEI parent data can look different from a cap table, a shareholding register, or a beneficial ownership chart. Those tools answer different questions.

Why ultimate parent information matters for LEI transparency

The ultimate parent field helps the LEI system answer a broader market question: who sits at the top of the reporting group behind this legal entity?

That makes LEI data more useful for banks, counterparties, regulators, trading venues, and internal compliance teams. A single LEI record stops being only a business card. It starts showing where the entity belongs in a larger corporate structure.

For Indian businesses dealing in bonds, derivatives, foreign investments, or other regulated market activity, accurate parent reporting can reduce friction during onboarding and periodic reviews. It also helps prevent awkward situations where two related entities appear unrelated on paper.

A well-reported parent structure supports:

- Better group transparency

- Faster validation checks

- Cleaner counterparty screening

- Fewer surprises at renewal

- Stronger confidence in reported data

How LEI Level 2 data records direct and ultimate parent relationships

The LEI system stores parent information in what is often called Level 2 data. Level 1 tells the market who the entity is. Level 2 adds the relationship layer and answers the question of who owns whom, within the accounting consolidation framework.

These parent links are not just free-text notes inside a record. They are structured relationship records. In simple terms, the child entity points to the parent entity through a specific relationship type.

Two relationship types matter most here. One signals that the entity is directly consolidated by another legal entity. The other signals that it is ultimately consolidated by another legal entity. This makes the difference between the closest parent and the top parent explicit.

The structure also carries context. That includes whether the relationship is active, when it was recorded or updated, and which validation basis was used.

Key LEI relationship fields include:

- StartNode: the child entity whose LEI record points upward

- EndNode: the parent entity identified in the relationship record

- RelationshipType: whether the link is direct consolidation or ultimate consolidation

- RelationshipStatus: whether the relationship is active or inactive

- RelationshipPeriods: the dates tied to the validity of the relationship

- Qualifiers: details that can include the accounting standard behind the relationship

- Registration metadata: dates, managing LOU, and validation information

This is one reason LEI data is useful beyond a one-time filing exercise. The structure allows systems and analysts to map group relationships at scale, not just read them manually.

It also explains why a parent name on its own is not enough. A robust LEI relationship needs the correct legal entity, the correct position in the chain, and the right reporting basis.

Why a shareholder is not always the ultimate parent in LEI data

This is where many reporting mistakes begin.

A majority shareholder may not be the ultimate parent for LEI purposes if that shareholder does not prepare consolidated financial statements including the entity. A holding arrangement may look decisive from a governance angle but still fail the LEI parent test. Likewise, a sponsor, promoter, or beneficial owner may matter greatly in other regulatory settings but may not appear as the LEI parent.

Take a private group where several entities are held by a family office or individual shareholders. If the top controlling party is a natural person, the LEI parent framework may not show that person as the ultimate parent because the LEI parent model is designed around legal entities and accounting consolidation.

That is why the question should not be, “Who controls us in a broad sense?” A better question is, “Which legal entity is the highest one that consolidates us in its financial statements?”

Common LEI exceptions when no ultimate parent is shown

Sometimes an LEI record does not show a direct parent, an ultimate parent, or both. That does not automatically mean the filing is wrong.

The LEI framework allows reporting exceptions where parent data cannot be disclosed or cannot be represented in the standard way. This is an important feature because corporate structures are not always neat, public, or LEI-ready.

You may see exceptions linked to issues like these:

- NO_LEI: the parent exists but does not have an LEI

- NATURAL_PERSONS: the controlling party is a natural person rather than a legal entity

- NON_CONSOLIDATING: there is no parent that consolidates the entity under the relevant accounting rules

- NO_KNOWN_PERSON: no controlling person is known in the required sense

- NON_PUBLIC: the relationship is not publicly available

For users reading LEI data, this is a valuable reminder. A blank parent field and an exception-backed absence are not the same thing.

For applicants, it means accuracy matters more than trying to force a parent into the record. A justified exception is better than an incorrect parent relationship that later needs correction.

How to identify the ultimate parent using LEI data

If you need to identify the ultimate parent of a company, the cleanest route is to start with the entity’s LEI and inspect its Level 2 relationship data.

Where the record includes an explicit ultimate consolidation relationship, the answer is direct. The parent named in that relationship is the ultimate parent for LEI purposes. If only the direct parent is visible in the tool you are using, you may need to move up the chain and confirm whether a higher consolidating entity exists.

A practical process looks like this:

- Find the company’s LEI record in a trusted LEI data source.

- Check whether a direct parent relationship is present.

- Check whether an ultimate parent relationship is present.

- If only the direct parent is obvious, review the parent’s own record and the broader group structure.

- Look for any reporting exception before assuming that no parent exists.

- Review update dates and status to make sure the relationship is current.

This is also why many public application portals focus on registration and renewal, not on full-scale ownership analytics. For deep group mapping, the official LEI data layer remains the best starting point.

Practical LEI filing tips for Indian entities reporting parent data

For Indian companies, LLPs, funds, trusts, charities, and other legal entities, the best approach is to prepare parent information before starting the LEI application. That saves time and reduces back-and-forth during validation.

The most reliable source is usually the latest audited or otherwise valid consolidated financial statements of the group. Board assumptions, informal organisation charts, and internal labels can point you in the right direction, but the LEI parent framework still comes back to consolidation.

If you are applying through a registration agent, a quick application flow is helpful, but speed works best when the parent details are already correct. LEI Service, for example, helps entities in India apply, renew, and transfer LEIs quickly with clear INR pricing and English-language support, yet the parent information still depends on the applicant’s actual consolidation facts and supporting records.

A few practical checks can make the process smoother:

- Use consolidated accounts first: they usually give the clearest answer on direct and ultimate parent positions

- Check whether the parent has an LEI already: if not, an exception may be needed rather than a missing field

- Match legal names carefully: group brand names and legal entity names are often different

- Review the chain from nearest to highest parent: this helps separate direct parent from ultimate parent

- Renew on time: parent relationships can become stale if entity data is not recertified

One more point matters for cross-border groups. An Indian subsidiary may have a direct parent in one country and an ultimate parent in another. That is normal. What matters is that the chain reflects the real consolidation structure and not just the local operating hierarchy.

Getting this right strengthens the quality of the global LEI data set and makes the entity easier to identify, validate, and trust in market activity.

And that is exactly what good LEI reporting is meant to do.