What Is an LEI Code? A Plain-English Guide for Indian Legal Entities

If your company, LLP, fund, trust, society, or other registered organisation deals with banks, securities markets, derivatives, or large-value payments, you may already have heard the term LEI. It can sound technical at first, but the idea is quite simple.

An LEI code is a global identity number for legal entities. It helps banks, regulators, investors, and counterparties confirm exactly who they are dealing with. For Indian entities, that matters not only for compliance, but also for smoother transactions, faster verification, and stronger credibility in domestic and cross-border finance.

What an LEI code means for a legal entity

LEI stands for Legal Entity Identifier. It is a unique 20-character alphanumeric code assigned to a legally registered entity that takes part in financial transactions. It follows the ISO 17442 standard and is designed to identify one entity, and only one entity, anywhere in the world.

The code itself is not a random label with no purpose attached to it. It connects to verified reference data about the entity, including its legal name, registered address, country of registration, and, where applicable, details about its parent relationships. This data is available through the Global LEI Index, which is supported by GLEIF, the Global Legal Entity Identifier Foundation.

In practical terms, an LEI answers two very useful questions: who is this entity, and who owns it. That may sound basic, yet in finance it solves a real problem. Many businesses have similar names, operate across jurisdictions, or sit within layered ownership structures. A standard global identifier cuts through that confusion.

An LEI is not the same as PAN, CIN, GSTIN, or IEC. Those identifiers remain important in India, but they serve different functions. The LEI is built for trusted entity identification in financial activity across institutions and borders.

Why Indian regulators ask for an LEI code

India has steadily brought LEI requirements into the financial system through RBI, SEBI, and IRDAI directions. The purpose is clear: better transparency, cleaner reporting, stronger risk control, and fewer identity errors in regulated transactions.

RBI has applied LEI requirements across several areas over time, including OTC derivatives, non-derivative markets, high-value payment systems, cross-border transactions, and corporate borrowing above specified exposure thresholds. SEBI has also brought LEIs into parts of the securities market, including certain issuers and foreign portfolio investors. IRDAI has introduced LEI-related requirements in insurance-linked contexts as well.

That means the question for many Indian entities is no longer “What is an LEI?” but “Do we need one now, before our next transaction or filing?”

| Situation in India | Why the LEI matters |

|---|---|

| RTGS or NEFT payments of ₹50 crore and above by non-individuals | RBI requires the LEI to be captured for these transactions |

| Cross-border capital or current account transactions of ₹50 crore and above | Banks may need the LEI before processing |

| Corporate borrowing above RBI exposure thresholds | Lenders collect LEI data and may refuse fresh facilities or renewals without it |

| Certain listed debt issuers and market participants | SEBI rules may require an LEI for issuance, reporting, or registration |

| Derivatives, money market, and government securities activity | LEI supports regulatory reporting and counterparty identification |

Rules can change, and banks may apply operational checks ahead of deadlines. So even where a mandate seems narrow, many entities choose to get their LEI in advance rather than wait for a payment, borrowing event, or market transaction to be held up.

Which Indian entities can get an LEI code

Any legal entity can apply for an LEI. An individual person cannot. The identifier is meant for legally recognised organisations and structures, whether they operate in finance directly or simply need the LEI to satisfy a bank or regulator.

This is one reason LEIs now appear across a wide range of sectors in India. They are not limited to listed corporates or large financial institutions. Charities, funds, educational bodies, and trade-focused entities may also need one if their activity touches regulated financial channels.

Common applicants include:

- Private limited companies

- Public limited companies

- LLPs and partnership firms

- Trusts, societies, NGOs, and charities

- Banks, NBFCs, insurers, and funds

- Government bodies, cooperatives, and statutory entities

If an entity enters into reportable financial transactions, raises money in regulated markets, deals in derivatives, makes very high-value payments, or is asked by a lender or custodian to furnish an LEI, eligibility is rarely the issue. Timing is.

Why an LEI code helps with compliance, due diligence, and market access

The immediate benefit is regulatory readiness. When an LEI is already active, banks and intermediaries can process applicable transactions without waiting for last-minute identification work. That can be especially useful where treasury teams, finance departments, legal teams, and counterparties are all working to a deadline.

There is also a strong operational benefit. A standard identifier reduces the need to repeatedly explain or evidence the same entity details across multiple systems. When the counterparty can validate your legal identity through a recognised global standard, onboarding and review can become more straightforward.

A third advantage is reputational. An active LEI signals that the entity’s core reference data is verifiable in a globally recognised system. That helps when dealing with overseas banks, international investors, custodians, and trade counterparties.

A few of the practical gains stand out:

- Regulatory readiness: fewer delays in bank processing, reporting, and market participation

- Counterparty clarity: one recognised identifier across jurisdictions

- Cleaner data: less confusion caused by similar entity names and inconsistent records

- Stronger trust: easier due diligence for lenders, investors, and overseas partners

For many Indian entities, the LEI has shifted from a technical compliance item to a useful part of financial infrastructure. It supports KYC, risk review, payment processing, securities activity, and cross-border business in one consistent framework.

How to apply for an LEI code in India

Applying for an LEI is usually much simpler than people expect. Most entities use an LEI registration agent or issuer channel that collects the required details, validates the information, and submits the application to a GLEIF-accredited Local Operating Unit.

A service like LEI Service is built around that process. The application can be started online in about a minute, pricing is shown in INR, GLEIF fees are included, and email support is available in English. There are also renewal, transfer, multi-year, and automatic renewal options, which can help entities that do not want to track expiry dates manually.

The basic process looks like this:

| Step | What you do | Usual time |

|---|---|---|

| Choose the application type | Select new LEI, renewal, or transfer | About 1 minute |

| Enter entity details | Fill in legal name, address, registration data, and authorised contact | 5 to 10 minutes |

| Upload documents | Submit the proof needed for validation | A few minutes |

| Make payment | Pay the fee online in INR | About 5 minutes |

| Validation and issuance | Data is checked and the LEI is issued if approved | Often 2 to 48 hours |

The exact documents depend on the entity type, but the principle is the same: the issuing side must be able to verify that the entity exists, that its legal details match official records, and that the applicant is authorised to act.

Typical documents include:

- Core identity proof: Certificate of Incorporation, registration certificate, partnership deed, trust deed, or equivalent

- Address proof: GST certificate, utility bill, lease document, or another accepted official record

- Tax or registration number: PAN, CIN, GSTIN, IEC, UDYAM, or another applicable identifier

- Authorised signatory details: the name and role of the person filing the application

For many Indian entities, data validation is quick when the name and address on the form exactly match the uploaded records. If the documents are clear and the details are consistent, issuance can be very fast. Some applications are processed within a few hours, especially when filed during working hours.

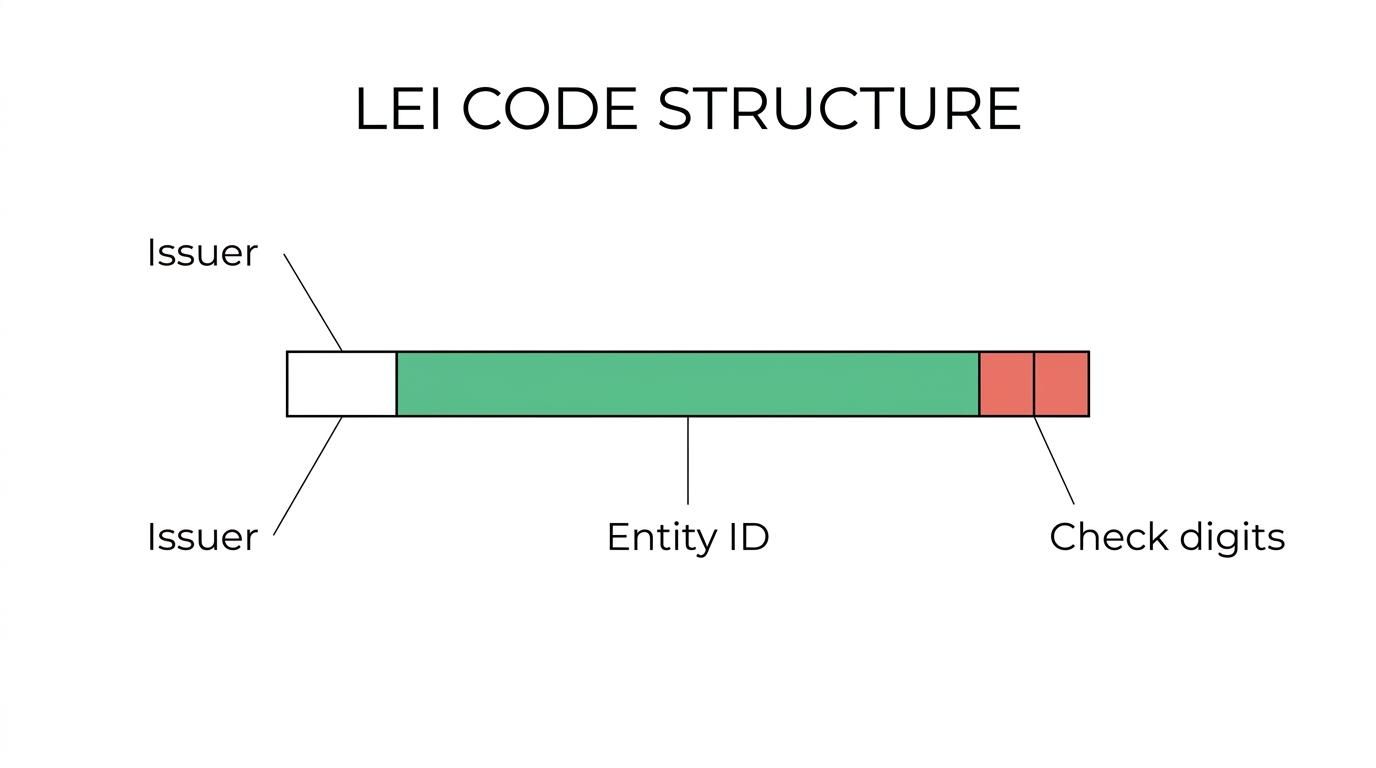

What the 20-character LEI code actually tells you

An LEI always contains 20 alphanumeric characters, but those characters are not meant to be read like an ordinary business code. One part identifies the issuing organisation in the LEI system, one part is entity specific, and the final two characters are check digits used for validation.

That structure matters because it supports uniqueness and reliability. The code is built to prevent duplication and reduce the risk of misidentification. Two entities cannot share the same LEI, and one entity should not have multiple LEIs.

This is why the LEI has become so useful in risk systems, reporting platforms, and payment data standards. It is clean, global, standardised, and machine-readable without losing its link to real-world legal records.

Why LEI renewal matters after registration

An LEI is not a one-time task that can be forgotten forever. It must be renewed every year to keep the linked reference data current. If it is not renewed, the code does not vanish, but its status can become lapsed. That can create problems where banks, exchanges, or counterparties expect an active LEI.

Renewal is really a data freshness check. The issuer or registration agent confirms that the entity details are still correct, or updates them where needed. If the registered address, legal name, or ownership details have changed, those changes should be reflected in the LEI record.

This is one reason automatic renewal can be useful for busy finance teams. A missed renewal date may appear minor internally, yet it can turn into a blocked process at exactly the wrong time, during a payment, a borrowing renewal, or a market transaction.

When to apply for an LEI code before a transaction

The best time to apply is before a transaction depends on it. That sounds obvious, but many entities still leave the LEI until a bank, custodian, exchange, or lender asks for it at the last moment.

A better approach is to apply when any of the following are on the horizon: a large domestic payment, a cross-border remittance, a new borrowing facility, a renewal of credit lines, a debt issuance, an FPI-related filing, or participation in a regulated market product. In those cases, having an active LEI already in place gives your team more room to focus on the transaction itself.

For Indian legal entities, the LEI is quickly becoming part of standard financial readiness. It is a small code with a very large job: proving, in a trusted and globally recognised way, exactly who your organisation is.